Understanding what employee benefits are legally required is one of the most critical responsibilities any employer faces. Failing to provide mandated benefits can expose your business to penalties, lawsuits, and damaged employee trust. This guide breaks down every major federal and state-level requirement so you can stay fully compliant.

According to the U.S. Department of Labor, employers must navigate a layered system of federal and state obligations when it comes to employee benefits. Some benefits are non-negotiable by law, while others are entirely voluntary. Knowing the difference protects both your workforce and your bottom line.

What Employee Benefits Are Legally Required? A Direct Answer

Quick Answer: Legally required employee benefits include Social Security and Medicare contributions (FICA), federal and state unemployment insurance, workers’ compensation coverage, FMLA unpaid leave (for eligible employers), and COBRA continuation health coverage. Additional mandates may apply depending on your state and company size.

In addition, the Affordable Care Act (ACA) requires employers with 50 or more full-time equivalent employees to offer minimum essential health coverage. Therefore, the exact list of mandatory benefits depends on your business size, location, and industry.

Employers must regularly audit their benefits programs to confirm all legally required employee benefits are in place.

Federal Mandated Benefits Every Employer Must Provide

Federal law establishes a baseline of benefits that most employers must offer. These requirements apply across all states, though state law can add further obligations on top of them.

1. Social Security and Medicare (FICA Taxes)

The Federal Insurance Contributions Act (FICA) requires both employers and employees to contribute to Social Security and Medicare. Specifically, employers must withhold 6.2% of each employee’s wages for Social Security and 1.45% for Medicare, then match those amounts dollar for dollar.

Furthermore, the employer’s matching contribution is a direct cost of employment. Consequently, this is one of the most universal mandated benefits — it applies to virtually every business with at least one employee.

2. Unemployment Insurance

Unemployment insurance (UI) is a joint federal-state program that provides temporary income to workers who lose their jobs through no fault of their own. Employers fund this program through payroll taxes under the Federal Unemployment Tax Act (FUTA) and corresponding state unemployment tax acts (SUTA).

As a result, even small businesses must register with their state’s unemployment agency and remit taxes regularly. The FUTA rate is 6% on the first $7,000 of each employee’s wages, though employers who pay state UI taxes on time receive a credit of up to 5.4%, reducing the effective federal rate to 0.6%.

3. Workers’ Compensation Insurance

Workers’ compensation provides wage replacement and medical benefits to employees who suffer work-related injuries or illnesses. In return, employees generally cannot sue their employer for negligence. Nearly all states require employers to carry workers’ compensation coverage, though the specific rules vary by state.

For example, some states allow employers to self-insure, while others require coverage through a state-run fund or private insurer. Failure to carry required coverage can result in severe fines and personal liability for the business owner.

Leave and Continuation Benefits Required by Law

4. Family and Medical Leave (FMLA)

The Family and Medical Leave Act (FMLA) requires covered employers to provide up to 12 weeks of unpaid, job-protected leave per year. Qualifying reasons include the birth or adoption of a child, a serious health condition, or caring for a family member with a serious illness.

However, FMLA applies only to employers with 50 or more employees within 75 miles of a worksite. Additionally, the employee must have worked for the employer for at least 12 months and logged at least 1,250 hours in the past year. Despite being unpaid leave, the employer must maintain the employee’s group health benefits during the leave period.

5. COBRA Continuation Coverage

COBRA — the Consolidated Omnibus Budget Reconciliation Act — requires employers with 20 or more employees who offer group health plans to allow employees and their dependents to continue health coverage after a qualifying event. Qualifying events include job loss, reduced hours, divorce, or the death of the covered employee.

Typically, COBRA coverage lasts up to 18 months, though some qualifying events extend it to 36 months. Importantly, the employee pays the full premium plus an administrative fee, but the continuity of coverage protects them during transitions.

Transparent communication about required and voluntary benefits builds trust with your workforce.

ACA Health Coverage: When It Becomes Mandatory

Under the Affordable Care Act (ACA), employers with 50 or more full-time equivalent (FTE) employees — known as Applicable Large Employers (ALEs) — must offer minimum essential health coverage to full-time employees and their dependents. This is often called the “employer mandate” or “shared responsibility provision.”

Specifically, the coverage offered must be affordable (employee premium cannot exceed a set percentage of household income) and must provide minimum value (covering at least 60% of total allowed costs). Employers who fail to comply face substantial penalties under IRS Section 4980H. According to the IRS, the penalty for 2024 is $2,970 per full-time employee beyond the first 30.

State-Mandated Benefits That Go Beyond Federal Law

Beyond federal requirements, many states impose additional benefit obligations. For example, California, New York, New Jersey, and several other states require employers to provide paid family leave or short-term disability insurance funded through payroll deductions.

Similarly, some states have enacted mandatory paid sick leave laws that require employers to provide a minimum number of paid sick days per year. Therefore, employers must research the specific laws in every state where they have employees — not just their headquarters state.

Furthermore, some states have introduced mandatory retirement savings programs. For instance, California’s CalSavers program requires employers who do not offer a qualified retirement plan to automatically enroll employees in the state-run IRA program.

How to Audit Your Business for Benefit Compliance

Staying compliant requires a proactive, systematic approach. Below is a step-by-step process to ensure your business meets all mandatory benefit obligations.

- Identify your employer size and classification. Count your full-time and part-time employees to determine which size-based thresholds apply to your business for FMLA, COBRA, and ACA purposes.

- Review all applicable federal benefit requirements. Audit your payroll setup for FICA withholding accuracy, verify FUTA payments, confirm FMLA policies are documented, and check ACA compliance if you have 50 or more FTEs.

- Check state-specific benefit mandates. Research every state where you employ workers. Look for paid family leave laws, short-term disability requirements, state unemployment tax obligations, and sick leave mandates.

- Update your employee handbook and benefit policies. Document all mandatory benefits clearly, including eligibility criteria, application procedures, and employee rights under each law.

- Consult an HR compliance specialist for ongoing review. Partner with a qualified HR advisor to conduct annual benefits audits and stay current with legislative changes at both the federal and state level.

For expert guidance on building a compliant and competitive benefits program, Soteria HR offers comprehensive HR compliance and benefits consulting services tailored to businesses of all sizes. For a deeper walkthrough, see our Labor Law Compliance: A Complete 2025 Guide for SMB Leaders.

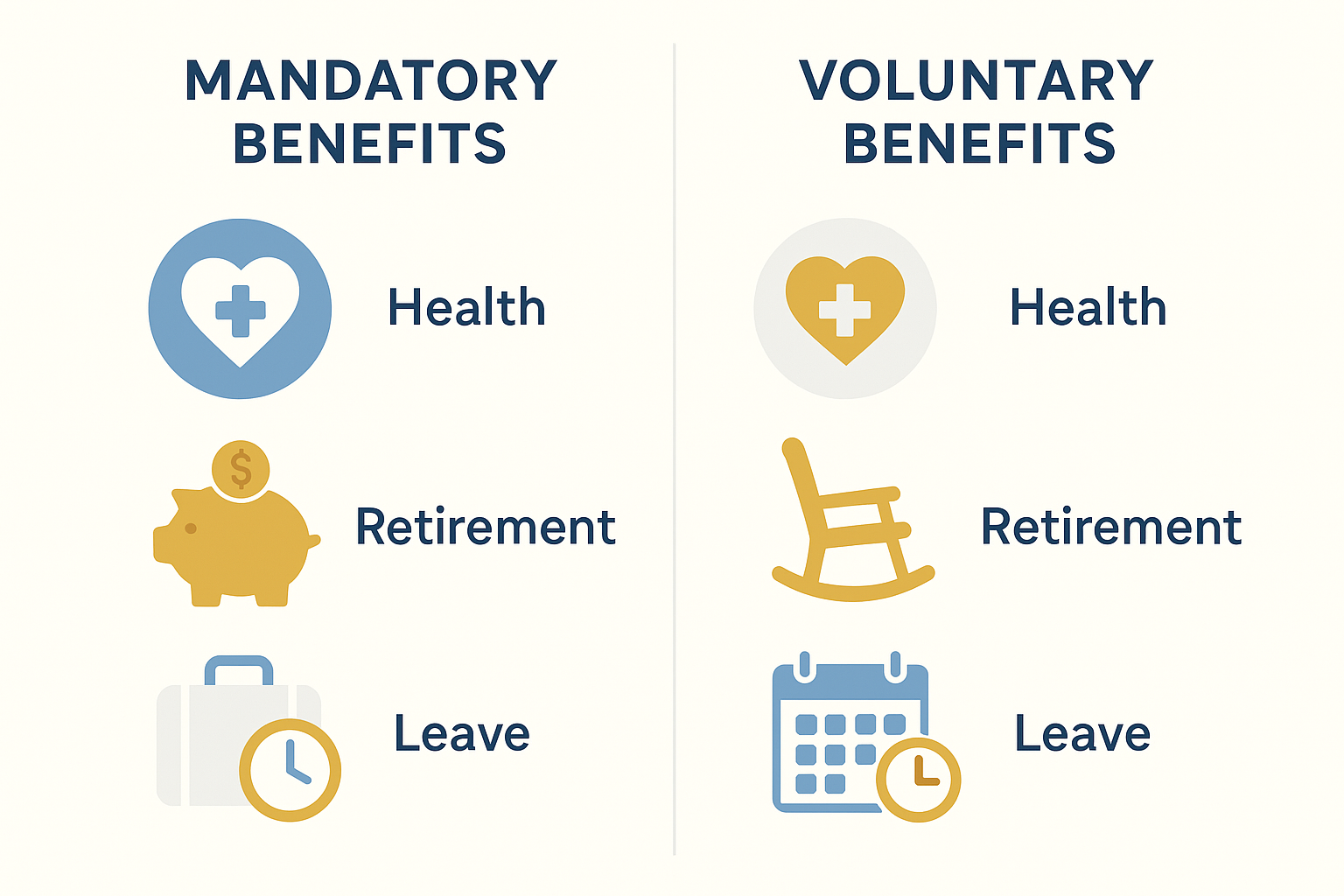

Mandatory vs. Voluntary Benefits: Understanding the Distinction

It is important to distinguish between benefits required by law and those offered voluntarily. Mandatory benefits — such as FICA, unemployment insurance, and workers’ compensation — are non-negotiable. Voluntary benefits, on the other hand, include offerings like dental and vision insurance, life insurance, 401(k) plans, and wellness programs.

However, voluntary benefits play a crucial role in talent attraction and retention. In fact, according to a SHRM survey, 60% of employees say benefits are a major factor in deciding whether to stay with an employer. To explore how voluntary benefits can strengthen your workforce strategy, visit our guide on voluntary employee benefits.

Additionally, combining a strong mandatory benefits foundation with thoughtful voluntary offerings is the hallmark of a well-rounded HR strategy. Learn more about building that foundation in our strategic benefits planning resource.

Understanding the difference between required and optional benefits helps employers build a compliant and competitive total rewards package.

Common Mistakes Employers Make With Required Benefits

Even well-intentioned employers sometimes fall short on compliance. Here are the most frequent errors to avoid:

- Misclassifying employees as independent contractors — contractors are not entitled to FICA matching, workers’ comp, or FMLA, so misclassification can create false savings that later become major liabilities.

- Ignoring state-level mandates — focusing only on federal law while overlooking state-specific paid leave or disability insurance requirements is a common and costly oversight.

- Failing to send COBRA notices on time — employers must provide COBRA election notices within 14 days of a qualifying event; late notices trigger penalties.

- Not tracking FMLA leave correctly — poor recordkeeping can lead to inadvertent FMLA interference claims, which carry significant legal exposure.

Frequently Asked Questions About Legally Required Employee Benefits

What employee benefits are legally required by federal law?

Federally required benefits include Social Security and Medicare contributions (FICA), unemployment insurance (FUTA), workers’ compensation, FMLA leave for eligible employers, and COBRA continuation coverage. Employers must provide these regardless of company size in most cases, though some thresholds apply.

Is health insurance a legally required employee benefit?

Health insurance is required under the ACA for employers with 50 or more full-time equivalent employees. Smaller employers are not federally mandated to offer health insurance, though some states have additional requirements.

Are employers required to offer paid vacation or paid time off?

No federal law requires employers to provide paid vacation or paid time off. However, if an employer chooses to offer PTO, state laws may govern how it is administered and whether unused time must be paid out upon termination.

What is COBRA and when is it required?

COBRA requires employers with 20 or more employees who offer group health plans to allow employees and their dependents to continue coverage after qualifying life events such as job loss or reduced hours. Coverage typically lasts up to 18 months.

Do small businesses have to provide the same mandatory benefits as large employers?

Not always. FMLA and COBRA only apply once an employer reaches certain headcount thresholds. However, FICA taxes and workers’ compensation requirements generally apply to businesses of all sizes.

What is FMLA and which employers must comply?

The Family and Medical Leave Act requires covered employers to provide up to 12 weeks of unpaid, job-protected leave per year. Employers with 50 or more employees within 75 miles of a worksite must comply.

Are state-mandated employee benefits different from federal requirements?

Yes. States can impose additional benefit requirements beyond federal law, such as paid family leave, short-term disability insurance, or expanded sick leave. Employers must comply with both federal and applicable state laws.

What happens if an employer fails to provide legally required benefits?

Failing to provide mandatory benefits can result in significant penalties, back-payment obligations, lawsuits, and regulatory investigations. FICA non-compliance can trigger IRS penalties, and FMLA violations may lead to employee lawsuits for damages.

Is workers’ compensation insurance mandatory for all employers?

Workers’ compensation requirements vary by state, but nearly all states require employers to carry some form of coverage. It provides wage replacement and medical benefits to employees injured on the job.

What is the difference between mandatory and voluntary employee benefits?

Mandatory benefits are required by law, such as Social Security contributions, unemployment insurance, and workers’ compensation. Voluntary benefits — like dental insurance or 401(k) plans — are offered at the employer’s discretion to attract and retain talent.

Do part-time employees get the same legally required benefits as full-time employees?

It depends on the benefit. FICA taxes apply to all employees regardless of hours worked. FMLA eligibility requires at least 1,250 hours worked in the past 12 months, which may exclude many part-time workers.

What is unemployment insurance and how does it work?

Unemployment insurance is a joint federal-state program providing temporary income to workers who lose their jobs through no fault of their own. Employers fund it through payroll taxes under FUTA and corresponding state unemployment tax acts (SUTA).

Are retirement plans legally required for employers?

No federal law requires private employers to offer retirement plans. However, some states have enacted auto-enrollment retirement savings programs that apply to employers who do not already offer a qualified plan.

Conclusion: Building a Compliant Benefits Foundation

Knowing what employee benefits are legally required is the foundation of responsible HR management. From FICA contributions and unemployment insurance to FMLA leave and COBRA coverage, each mandated benefit exists to protect workers and ensure fair treatment across the workforce. Furthermore, state-level mandates add another layer of complexity that employers cannot afford to ignore. By conducting regular compliance audits, staying informed about legislative changes, and partnering with experienced HR professionals, your business can meet every obligation — and build a benefits program that genuinely supports your team. For tailored compliance support, explore the resources available at Soteria HR.